29 Apr 2024

Investor sentiment continues to be hobbled by a higher-for-longer US interest rate outlook. This makes this Q1 earnings season especially important. On this front, results have been mixed so far, with Q1 EPS growth now expected at just 0.5% year-on-year, lower than the 3.4% predicted as recently as last month. It’s still early days and a lot will hinge on the performance of the ‘Magnificent Seven’ technology mega-caps.

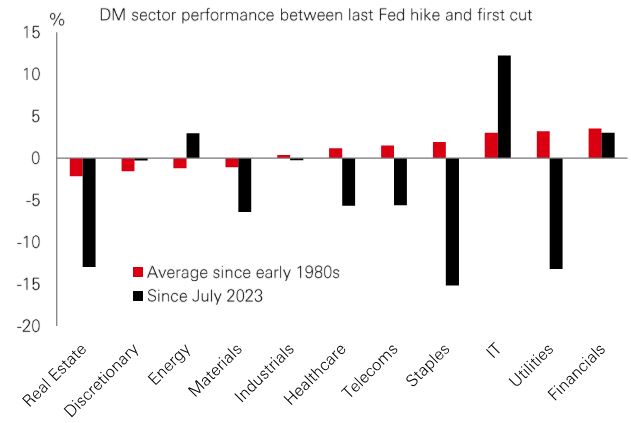

US profits expectations for the full year 2024 have been on an improving trend over the past few months. This has come amid ongoing economic resilience. And analysts expect EPS growth to become less dependent on the big tech names as the year progresses.

Most EM stock markets have seen a downward trend in earnings revisions. This divergence reflects the strain of higher-for-longer Fed rates, as well as FX volatility caused by the strong US dollar.

But it’s not all bad. Q1 earnings in Asia have so far modestly surprised to the upside. Trade flows are improving amid a recovery in chip demand. And policy support in mainland China is showing signs of success. If that continues, the earnings outlook can stabilise.

Frontier market stocks have been caught up in the global equity sell-off this month. Nevertheless, the drawdown has been relatively minor (-4%) despite the prospect of higher-for-longer US rates weighing on performance.

One possible reason for this is that the frontier basket benefits from low intra-country correlations. This implies diversified performance and lower volatility. Frontier markets are generally dominated by domestic investors with idiosyncratic local issues also driving sentiment, and are relatively under-owned by global investors (and seemingly undervalued).

But that’s not all. Correlations vis-a-vis EMs and DMs are also low, making exposure a potential source of portfolio diversification. Frontiers are also some of the world's fastest growing economies – including Asian giants such as the Philippines and Vietnam (22% and 16% of MSCI Frontier Emerging, respectively). The former is expected to see further benefits from ‘friend-shoring’, while the latter is expected to lead the way in Asia’s policy easing cycle.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 11.30am UK time 26 April 2024.

Gold has broken higher since the start of March, rising by as much as 15%. Renewed concern about persistent inflation is likely to have played a role, given that gold has historically been an inflation hedge. But gold also tends to benefit from investor anxiety, which has been rising on recent geopolitical tensions.

On a more structural basis, gold has done well recently as investors confront longer-term challenges such as climate change, economic fragmentation, and resource nationalism – which are all inflationary and raise economic uncertainty. We have also seen major EMs diversify their FX reserves away from dollar-denominated assets amid geopolitical tensions and discomfort with the US fiscal position.

One consequence of these developments is that the historically close inverse correlation between the gold price and real US Treasury yields has, for now, broken down. This is one reason to be cautious on the yellow metal even if it is likely to remain in favour by investors looking for a potential portfolio hedge in the ‘multi-polar world’.

The classic 60/40 stock-bond portfolio – which balances upside exposure to equities with the downside protection of bonds – has been a historically reliable way of delivering solid risk-adjusted returns. But it stopped working in 2022, as the two usually uncorrelated assets both fell. Amid elevated inflation and an uncertain outlook, the risk of persistently high stock-bond correlations has been cited as a reason to give up on the strategy.

But its death seems greatly exaggerated. Last year, the 60/40 saw a solid gain of 18% on a total return basis and is up year-to-date. In part, that’s been driven by a rebound in stocks. But with the market pricing-in a higher-for-longer rates outlook, bond yields remain elevated. This makes the income component from bonds a meaningful source of returns in the mix.

And if we get an adverse growth shock or policy rate cuts, there is potential for capital gains from bonds. What will be crucial, however, is further progress on disinflation. This would bring back the idea of central bank ‘policy puts’ that can lower the stock-bond correlation.

Against a backdrop of a growing number of global central banks cutting interest rates, headlines about a surprise rate hike in Indonesia last week were attention-grabbing. Bank Indonesia Governor Warjiyo justified the decision to raise interest rates to 6.25% as a response to “worsening global risks” and as a “pre-emptive and forward-looking” measure to assert inflation control.

Across Asia, the key macro discussion is about the implication of higher-for-longer US interest rates and the stronger oil price. A hawkish Fed and ‘king dollar’ push Asian currencies lower and casts doubt over any rate cutting cycle.

Recent data in Asia have shown some modest inflation surprises, and favourable base effects are set to fade during Q2. That means that there is little urgency for Asian central banks to follow the lead of the LatAm and East European early rate cutters. Crucially, last week’s BI move shouldn’t be seen as a turn in strategy back to rate hikes; that’s not warranted on growth and inflation trends. Instead, the Asia rate cut cycle looks delayed and, when it comes, could be shallower than analysts had assumed.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 11.30am UK time 26 April 2024.

Source: HSBC Asset Management. Data as at 11.30am UK time 26 April 2024.

Rising US inflation worries weighed on core government bonds, with risk markets resilient and the DXY index softer. The US core PCE deflator surprised on the upside in Q1 2024, reinforcing the current market narrative of higher-for-longer US rates ahead of FOMC meeting this week. US equities posted decent gains in choppy trading amid mixed Q1 earnings. The Euro Stoxx 50 index eked out small gains on improving sentiment towards the eurozone economy. Broad-based yen weakness boosted the Nikkei as the BoJ left policy on hold in April, with the FY24 inflation forecast upgraded to 2.8%. In EM, the Shanghai Composite index fell modestly, but India’s Sensex remained in positive territory. In commodities, oil snapped a two-week losing streak on persistent supply concerns. Easing geopolitical concerns weighed on gold.

WARNING: THE CONTENTS OF THIS DOCUMENT HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN THE PEOPLE’S REPUBLIC OF CHINA OR ANY OTHER JURISDICTION. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

This document has been issued by HSBC Bank (China) Company Limited (the “Bank”) in the conduct of its regulated business in China. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment [in any jurisdiction in which such an offer is not lawful] or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Bank (China) Company Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. Do not rely on it for any investment or financial decisions.

The Bank and HSBC Group and/or their officers, directors and employees may have positions in any securities or financial instruments mentioned in this document (or in any related investments) (if any) and may from time to time add to or dispose of any such securities or financial instruments or investments. The Bank and its affiliates may act as market maker or have assumed an underwriting commitment in the securities or financial instruments discussed in this document (or in related investments) (if any), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services for or relating to those companies.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Investment schemes are subject to market risks. You should read all scheme related documents carefully.

Copyright © HSBC Bank (China) Company Limited 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Bank (China) Company Limited