24 Apr 2024

Tourism, as we know it, is changing in the face of rising temperatures and extreme weather events. Particularly in coastal tourism a stormy future looms as climate impacts, including rising sea levels, put its resilience to the test. We think adaptation measures will play an important role in keeping vulnerable coastal tourism afloat.

In this issue of #WhyESGMatters, we discuss the likely impacts of heat stress on global tourism, with a particular focus on coastal tourism. We also look at various adaptation methods that countries can implement to reduce the impacts from climate change.

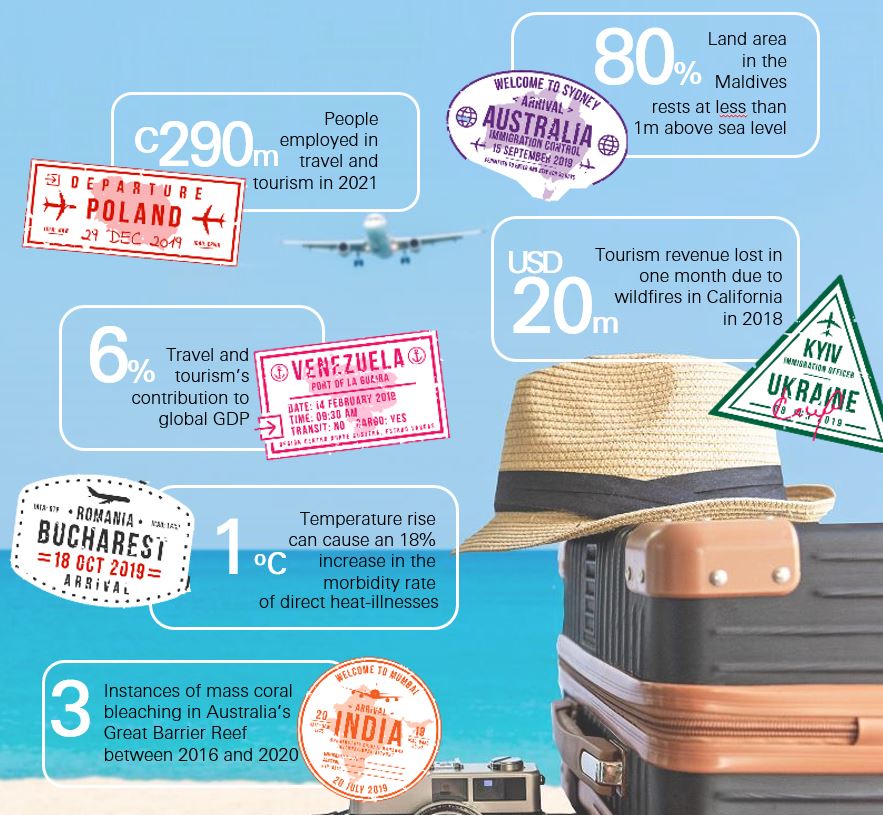

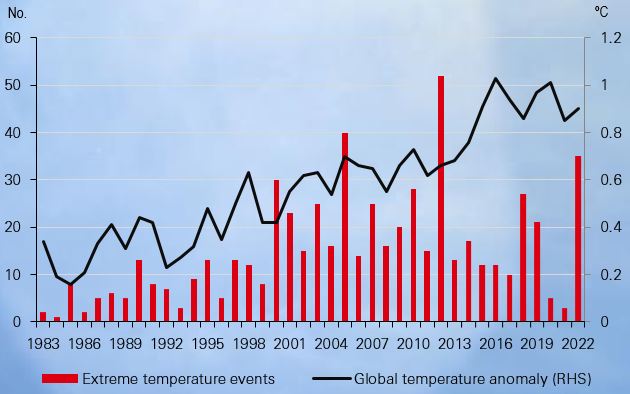

The travel and tourism industry, which contributed nearly 6% of global GDP and employed nearly 290m people in 2021 (as per the World Travel & Tourism Council), faces a myriad of challenges due to extreme temperatures (Figure 1). Relentless heatwaves pose serious health risks, such as dehydration and heatstroke, deterring tourists from venturing outdoors and hampering the industry’s usual vibrant activity.

An article published in the journal Science of the Total Environment in 2022 highlights evidence that a 1°C rise in temperature can lead to an 18% increase in direct heat illness morbidity. Further, smaller and less affluent economies may struggle to cope with mounting cooling demand, as travellers seek respite from the scorching heat. The heightened demand for air-conditioned spaces is also likely to cause a sharp increase in energy consumption, putting strain on local energy grids and increasing emissions.

Figure 1. Global warming is likely to increase the number of extreme temperature events

On the move

Sweltering weather is affecting travel plans. In July last year, the European Travel Commission (ETC) reported a decline in travel intent in Europe compared to previous years. Additionally, the popularity of Mediterranean destinations was found to have declined by 10% compared to the year before. On the other hand, destinations such as Bulgaria and Denmark are becoming increasingly popular due to their milder temperatures.

Although there is uncertainty about how tourists will respond to the effects of a changing climate, various popular tourist spots are likely to lose their appeal, paving the way for some lesser-known destinations to shine. This shift in traveller sentiment is likely to have a considerable impact on economies that rely heavily on tourism income.

Beaches are popular holiday destinations, accounting for nearly 50% of global tourism. However, coastal tourism is facing an imminent threat due to climate change. The industry is the economic backbone for some of the world’s poorest economies, including the Small Island Developing States (SIDS), which are also among the most vulnerable to climate change.

While extreme weather events, such as cyclones and floods, have already posed immediate risks, it’s rising sea levels and ocean acidification that are setting alarm bells ringing. Moreover, secondary impacts, such as water availability and the spread of diseases, are also a growing concern for coastal communities and travellers alike.

Sea level rise

Many popular tourist spots, such as the Maldives, are at risk of being submerged due to rising sea levels. Indonesia also announced plans in 2019 to relocate its capital from Jakarta in response to the threat posed by rising sea levels. Global sea levels have already risen by 98.5mm since 1993, according to NASA. Furthermore, the average rate of rise is accelerating, tripling from 1.3mm/year between 1901 and 1971 to 3.7mm/year between 2006 and 2018[@heat-on-holidays-01]. While the extent of sea level rise depends on emissions and uptake of heat by the oceans, 1bn people could be exposed by 2050[@heat-on-holidays-02]. And by 2100, extreme sea level events that previously occurred once per century could strike at least once a year on many coasts[@heat-on-holidays-03].

Unfortunately, even under a low CO2 emissions pathway, the world may lose 53% of its sandy beaches, on average, resulting in a loss of 30% of hotel rooms and a 38% decline in tourism revenue by 2100[@heat-on-holidays-04]. The imminent risks of shorelines being eroded, tourism infrastructure being inundated, and an increased likelihood of extreme weather events could lessen the recreational value of popular coastal tourist spots, potentially affecting business operators, such as resorts and hotels, water sports and tour operators (snorkelling and diving), ports and airlines.

Marine heatwaves and ocean acidification

The increased intensity and frequency of marine heatwaves are likely to cause coral reefs to undergo irreversible changes and disrupt marine life, affecting the character of the coastal landscape. For example, a recent marine heatwave that started to emerge in June last year along the coast of Queensland in Australia is raising concerns for the already vulnerable Great Barrier Reef.

The World Economic Forum[@heat-on-holidays-05] has estimated that 50% of the world’s coral reefs would be under threat by 2035 in the absence of climate risk mitigation. This presents a daunting challenge for coastal tourism as marine exploration activities, such as scuba diving, rely heavily on these vibrant underwater ecosystems.

Growing risk

Rising temperatures will significantly impact other tourism sub-sectors too:

The COVID-19 pandemic exposed the vulnerability of the tourism sector. Poor countries that heavily rely on tourism are poised to face significant challenges, including social unrest, as the flow of tourists slows due to impacts of a warming climate.

Adaptation measures, better forecasting and early-warning tools, and disaster risk management will play an important role in the tourism sector’s response to the impending risks. Infrastructure, such as seawalls and breakwater structures, and conservation of natural systems, such as mangroves, are important coastal protection measures.

Accommodation strategies, such as elevating key infrastructure and houses, can help reduce the impact of flooding. For instance, elevated houses built 1.5m above ground are subsidised by the government in the Tuamotu Archipelago, which is extremely prone to flooding.

Several regions have also been adopting ecosystem-based measures to respond to climate change. Artificial reefs have been increasingly used to support reef restoration in countries such as Antigua and Grenada. In Vanuatu, tourism businesses have been involved in establishing marine-protected areas to address climate-related risks.

As the impact of climate change continues to escalate, adaptation measures will become increasingly crucial in safeguarding vulnerable regions. However, we think it’s imperative to acknowledge that long-term resilience relies on a broad-based approach, combining adaptation strategies with global efforts to substantially reduce greenhouse gas emissions.

Rising emissions and climate change pose additional challenges beyond the immediate heat issues. In this note, we explored a range of other climate change impacts on the tourism sector, with a focus on coastal tourism. We think governments, businesses and investors must plan collaboratively for the long term – assessing exposure and working towards transformational adaptation to safeguard the tourism industry.

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Bank (China) Company Limited, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (200801006421 (807705-X)), The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, HSBC Private Bank Suisse SA, South Africa Representative Office, HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA, HSBC FinTech Services (Shanghai) Company Limited and The Hongkong and Shanghai Banking Corporation Limited and HSBC Mexico, S.A. Multiple Banking Institution HSBC Financial Group (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/business. However, the Bank disclaims any guaranty on the management or operation performance of the trust business.

The following statement is only applicable to by HSBC Bank Australia with regard to how the publication is distributed to its customers: This document is distributed by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL/ACL 232595 (HBAU). HBAP has a Sydney Branch ARBN 117 925 970 AFSL 301737.The statements contained in this document are general in nature and do not constitute investment research or a recommendation, or a statement of opinion (financial product advice) to buy or sell investments. This document has not taken into account your personal objectives, financial situation and needs. Because of that, before acting on the document you should consider its appropriateness to you, with regard to your objectives, financial situation, and needs.

The following statement is only applicable to HSBC Mexico, S.A. Multiple Banking Institution HSBC Financial Group with regard to how the publication is distributed to its customers: This publication is distributed by Wealth Insights of HSBC México, and its objective is for informational purposes only and should not be interpreted as an offer or invitation to buy or sell any security related to financial instruments, investments or other financial product. This communication is not intended to contain an exhaustive description of the considerations that may be important in making a decision to make any change and/or modification to any product, and what is contained or reflected in this report does not constitute, and is not intended to constitute, nor should it be construed as advice, investment advice or a recommendation, offer or solicitation to buy or sell any service, product, security, merchandise, currency or any other asset.

Receiving parties should not consider this document as a substitute for their own judgment. The past performance of the securities or financial instruments mentioned herein is not necessarily indicative of future results. All information, as well as prices indicated, are subject to change without prior notice; Wealth Insights of HSBC Mexico is not obliged to update or keep it current or to give any notification in the event that the information presented here undergoes any update or change. The securities and investment products described herein may not be suitable for sale in all jurisdictions or may not be suitable for some categories of investors.

The information contained in this communication is derived from a variety of sources deemed reliable; however, its accuracy or completeness cannot be guaranteed. HSBC México will not be responsible for any loss or damage of any kind that may arise from transmission errors, inaccuracies, omissions, changes in market factors or conditions, or any other circumstance beyond the control of HSBC. Different HSBC legal entities may carry out distribution of Wealth Insights internationally in accordance with local regulatory requirements. HSBC specifically prohibits the redistribution of this material and is not responsible for any actions that third parties may take to and/or with it.

Mainland China

In mainland China, this document is distributed by HSBC Bank (China) Company Limited (“HBCN”) and HSBC FinTech Services (Shanghai) Company Limited to its customers for general reference only. This document is not, and is not intended to be, for the purpose of providing securities and futures investment advisory services or financial information services, or promoting or selling any wealth management product. This document provides all content and information solely on an "as-is/as-available" basis. You SHOULD consult your own professional adviser if you have any questions regarding this document

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

The material contained in this document is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HSBC India does not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investments are subject to market risk, read all investment related documents carefully.

Important information on ESG and sustainable investing

In broad terms “ESG and sustainable investing” products include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors to varying degrees. Certain instruments we classify as sustainable may be in the process of changing to deliver sustainability outcomes. There is no guarantee that ESG and Sustainable investing products will produce returns similar to those which don’t consider these factors. ESG and Sustainable investing products may diverge from traditional market benchmarks. In addition, there is no standard definition of, or measurement criteria for, ESG and Sustainable investing or the impact of ESG and Sustainable investing products. ESG and Sustainable investing and related impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the ESG / sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of ESG / sustainability impact will be achieved. ESG and Sustainable investing is an evolving area and new regulations are being developed which will affect how investments can be categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.

© Copyright 2024. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document or video may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.