The importance of retirement planning for women

24 March 2023

Among the retired women involved in a survey carried out by YouGov for HSBC1, over 90% said they need up to £30,000 (around USD38,500) a year to fund their lifestyle. However, for many women, this amount is difficult to obtain. Another 29% stated that they don’t have enough money to make ends meet. A further 10% said their retirement savings aren’t enough to cover household bills, while 30% of respondents can’t afford to run a car.

Retirement planning is critical for women worldwide

Although these numbers may vary from country to country, it does serve as a wake-up call to all women regardless of where you live. Globally, the gender pay gap is improving, but women generally earn less than men throughout their careers, which limits the amount they can save for retirement. For example, women are more likely to take career breaks or reduce their working hours to look after children or elderly parents, thereby affecting their pension contributions and retirement income.

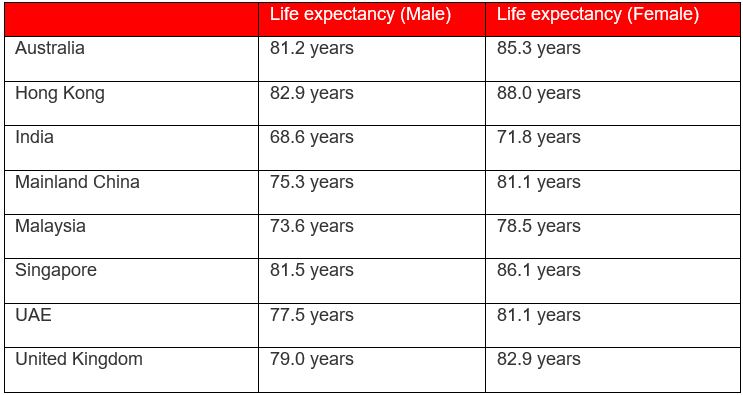

As women live longer, they need retirement income for longer

Life expectancy has also increased, with women generally living some four to eight years longer than men, due partially to more male smoking and drinking alcohol, physical stress with simultaneous aversions to medical treatment and health precautions, as well as genetic reasons2. Therefore, any retirement income may need to stretch further over a longer period of time for women. This fact shouldn’t be under-estimated. The earlier you start saving for your retirement, the more likely you are to:

-

be financially independent

-

have sufficient funds available to support the lifestyle you want

-

be able to cover an unexpected expense after you stop working

5 ways to boost your retirement savings

Taking action feels good. Here are some positive changes you can make today for a more comfortable retirement.

1. Maximise your pension contributions

If you can, now is the time to add as much as possible to your workplace pension or your retirement savings and make the most of tax relief from the government. Some employers offer to match your contributions up to a certain limit – if yours does, try to make the most of it.

If you’ve taken a career break, you may have gaps in your retirement savings. It may be possible to make voluntary contributions to make up for these.

2. Save more by making small changes

Take a look at your budget to see where you could potentially free up money. The more you save now, the more you’ll have to retire with.

3. Consider investing

Investing is an alternative way to save for your future, and could potentially provide higher long-term growth than leaving your money in a savings account, and help you combat inflation. The key difference is there are no guarantees as the value of investments can go down, as well as up, and you may not get back what you invest.

4. Make the most of joint allowances

If you’re married, in a civil partnership or in a stable relationship with shared assets, you may want to look at both your pensions and savings together. Try to work out the cost of living together when you’re no longer working.

5. Adjust your retirement plans

If you’re near retirement age and are concerned you won’t have enough money, think about whether you can delay when you finish work. If that’s an option, let your pension provider know as it may make sense to change the ways in which your pension is invested.

Switching to reduced working hours or ‘semi-retirement’ can also give you more financial security, as well as a better work-life balance.

Notes: 1/All figures, unless otherwise stated, are from YouGov Plc for HSBC. Total sample size was 1,048 retirees and 2,695 non-retirees, ranging from ages 18 to 55+. Fieldwork was undertaken between 5th and 6th January 2022. The survey was carried out online. The figures have been weighted and are representative of all Great British adults (aged 18+). 2/ WorldData.com - https://www.worlddata.info/life-expectancy.php

Related insights

Important information

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Bank Canada, HSBC Bank (China) Company Limited, HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (127776-V) / HSBC Amanah Malaysia Berhad (807705-X), The Hongkong and Shanghai Banking Corporation Limited, India, HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, HSBC Private Bank Suisse SA, South Africa Representative Office, HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA and The Hongkong and Shanghai Banking Corporation Limited (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful. The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/ business. However, the Bank disclaims any guarantee on the management or operation performance of the trust business.

© Copyright 2023. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.