22 Apr 2024

The recent escalation of events in the Middle East puts geopolitical risk back on the radar for global investors. Typically, geopolitical shocks – and a higher geopolitical risk premium – mean spikes in market volatility, higher correlations among risky assets, and risk-off moves favouring safe-havens.

But history also tells us that most geopolitical events have short-lived effects on markets. The general pattern is for an initial wobble in stocks, followed by market gains. But there is a caveat: some geopolitical events have resulted in much bigger-than-average stock market drawdowns. And several have had much longer durations.

The 1973 Oil Crisis stands out as a far-reaching and highly impactful event for investment markets. The shock tipped the world into recession in 1973-5, and toward a stagflation equilibrium.

In the current situation, the good news is that Saudi Arabia, Kuwait, and the UAE are sitting on more than 5m b/d of spare capacity, implying room to replace lost Iranian barrels. The US and China also have strategic reserves, and shale is now a big factor in US energy independence. Western economies are less oil-intensive than they were in the 1970s.

Increased market volatility may create an opportunity for contrarians to get long on risk assets. But at this juncture, risk premiums embedded in many Western asset classes look low. Elevated geopolitical risk is likely to be a feature, not a bug, of the ‘multi-polar’ international system.

Over the past six months, bonds issued by emerging markets with the B and C rated buckets (lowest credit ratings) have returned 14% and 46% respectively versus a total return of 10% for the broader Emerging Market Bond Index.

Three factors have driven outsized returns. First, lower food and energy prices have helped improve terms of trade allowing economies to return to growth and easing external financing needs. Second, support from international financial institutions has lowered credit risks in countries like Egypt and Pakistan, and in some cases, even allowed countries like Kenya to return to international capital markets. Finally, new governments have pivoted to sustainable policies in Türkiye, Argentina, and Ecuador.

The punchline here is with more sustainable policies and IMF programs in place, outperformance in these idiosyncratic stories can continue even in a challenging macro environment for fixed income.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 11am UK time 19 April 2024.

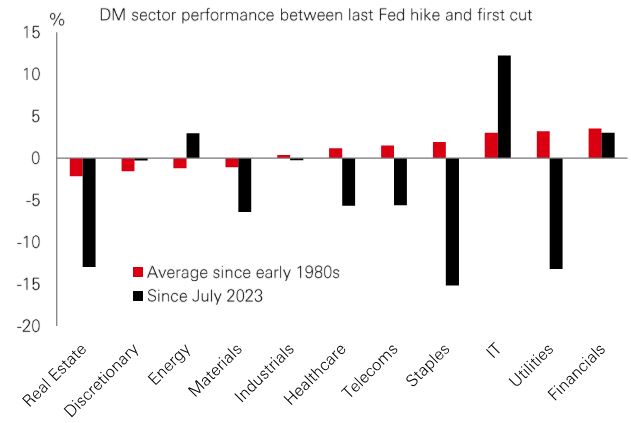

Since the Fed’s last rate hike in July 2023, defensive sector stocks – usually classic safe-havens – have been some of the market’s biggest losers. Relative sector performance in past cycles suggests that’s unusual. Since 1984, sector winners between the last hike and first cut have been, on average, Staples, Utilities, Technology and Financials. While Tech has been a big winner this time, the two defensives – Staples and Utilities – are both down by around 15%.

Today, Developed World Staples offer an excess dividend yield of 110 bps versus the market – about five times the 20-year average. Utilities offer an excess yield of 70 bps. And in the US, it’s only the second time in 40 years that the price-book ratio of Staples is below the market.

For investors, this relative underperformance could point to a source of cheap protection against adverse economic outcomes. And even in the absence of growth shocks, further disinflation and lower bond yields would likely benefit these sectors.

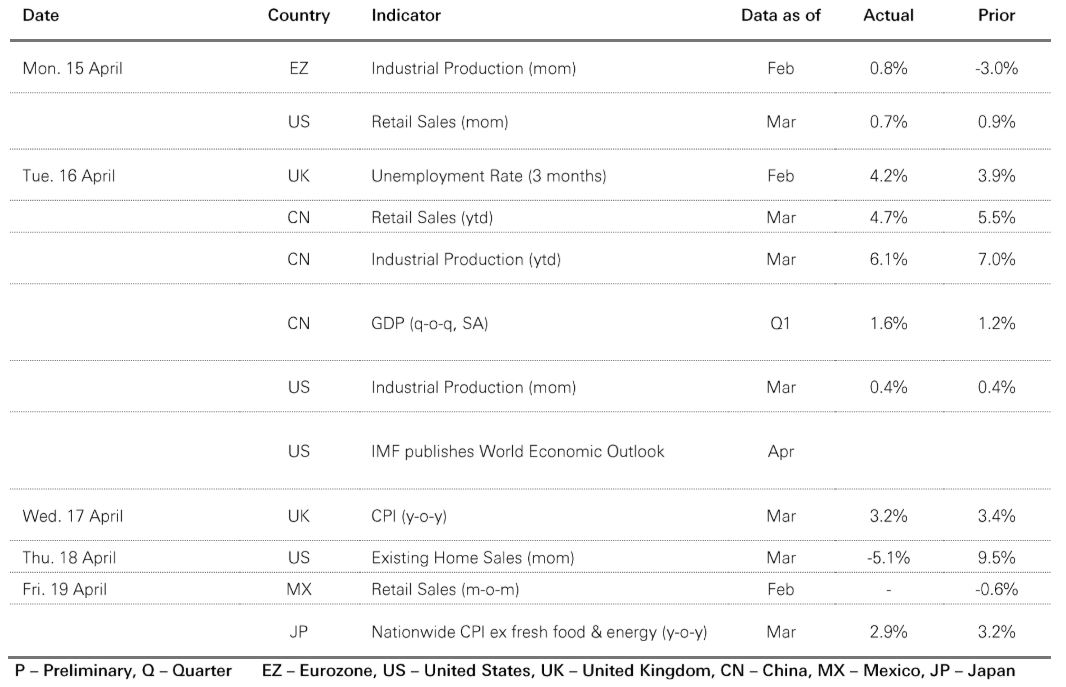

The latest IMF World Economic Outlook (WEO) forecasts highlight the widening divergence between growth in the US and other developed market economies. The IMF revised up its 2024 US GDP projection by 0.6pp to 2.7%. Europe was revised lower, Japan left unchanged, with both expected to grow by less than 1%.

This outperformance of US growth, and concerns that it may further hamper any progress on the inflation front, is playing out in bond markets and spilling into risk markets. The 10-year US Treasury yield has jumped by around 40bp since end-March as investors revise their assumptions around the timing of Fed rate cuts. This has coincided with a 5% month-to-date drawdown in the S&P 500.

And although strong US growth supports the domestic earnings and defaults outlook, limiting the downside, investors need to monitor the potential spillover effects to the rest of the world. In particular, the recent surge in the US dollar will have important implications, not least crimping the ability of many global central banks to ease policy.

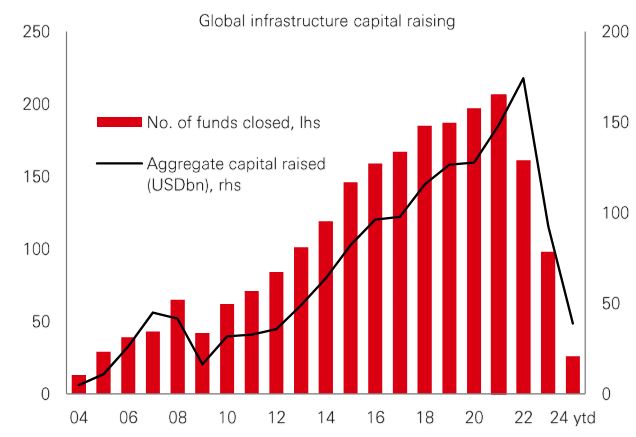

With assets under management of USD1.3 trillion, global infrastructure has been a popular asset class with investors in recent years. While elevated rates and lower deal activity saw fundraising slow and fewer new funds reach target (and close) in 2023, demand for private investment is expected to stay high.

Much of this private capital is earmarked for funding projects in the West. But infrastructure plans in Asia – particularly the region’s efforts to develop new renewable energy generation – are also a key opportunity, and one that could be overlooked by investors.

Asia tends to be unsuitable (and ignored) by large funds that need to invest at scale. That gives mid-market (sub-USD 1bn) funds a broader range of up-front opportunities in smaller projects. It also gives them the ability to have closer involvement in those projects, and more options when it comes to unwinding their exposure later on.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 11am UK time 19 April 2024.

Source: HSBC Asset Management. Data as at 11am UK time 19 April 2024.

Geopolitical concerns and US rate worries continue to weigh on risk markets. US government bonds were supported by safe-haven flows, with Fed Chair Powell acknowledging that US inflation “will likely take longer” to reach the 2% medium-term target. Further strong US data reinforced market expectations of just one to two rate cuts by year-end. US equities weakened across the board as investors digested Q1 earnings, while the Euro Stoxx 50 index moved sideways. Japan’s Nikkei 225 fell in choppy trading, with the yen stabilising against the US dollar. In EM, the Shanghai composite index rallied on supportive official comments over new investor-friendly stock market rules, while India’s Sensex index fell. In commodities, oil prices declined during last week as traders weighed the impact of Middle East tensions. Gold continues to hover around all-time highs.

WARNING: THE CONTENTS OF THIS DOCUMENT HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN THE PEOPLE’S REPUBLIC OF CHINA OR ANY OTHER JURISDICTION. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

This document has been issued by HSBC Bank (China) Company Limited (the “Bank”) in the conduct of its regulated business in China. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment [in any jurisdiction in which such an offer is not lawful] or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Bank (China) Company Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. Do not rely on it for any investment or financial decisions.

The Bank and HSBC Group and/or their officers, directors and employees may have positions in any securities or financial instruments mentioned in this document (or in any related investments) (if any) and may from time to time add to or dispose of any such securities or financial instruments or investments. The Bank and its affiliates may act as market maker or have assumed an underwriting commitment in the securities or financial instruments discussed in this document (or in related investments) (if any), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services for or relating to those companies.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Investment schemes are subject to market risks. You should read all scheme related documents carefully.

Copyright © HSBC Bank (China) Company Limited 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Bank (China) Company Limited