17 Jan 2024

Indonesiais facing elections amid growth that’s set to tick along, and could see householdspending pick up steam. Thailandis grappling with weak investment, but fiscal easing offers a welcome boost. Malaysia should see improvements aswell, helped by steadying exports. The Philippines is on course to deliver another impressive year, achieving the second-highest growthrate in ASEAN, after Vietnam, which should enjoy a snap-back from a challenging 2023. Singapore,meanwhile, more exposed to global fluctuations than most, should benefit as well from stabilisingdemand across the region in 2024.

It’s politics... Indonesia will have a new president in 2024, given President Jokowi cannot stand again due to a two-term limit. The leading presidential candidate must secure 50% of the votes in the 14 February elections; otherwise, there will be a run-off on 26 June. Prabowo Subianto is leading in the polls currently, and, while under 50%, his share of the vote looks to be rising (Lembaga Survei Indonesia, November 2023).

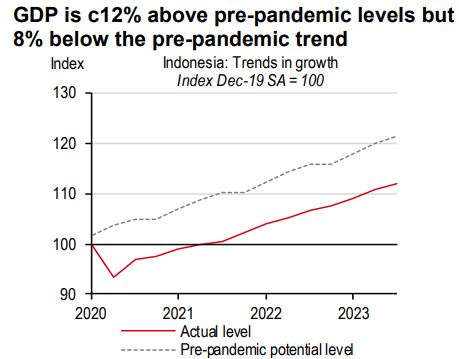

But not just politics. Even the state of the economy could change in 2024. Recall that Indonesia was an oasis of stability in the last few years, with inflation, the current account and fiscal deficit, all under control. What gave way was the growth recovery. As evidenced by tepid credit growth, GDP growth was soft (e.g. 4.9% in the September quarter versus 5.3% potential growth), led by tight fiscal and monetary policy, and exacerbated by China’s soft recovery, which is an important trade partner.

In fact, weak credit growth was a key reason for the macro stability Indonesia enjoyed. Firstly, low credit growth means that much of the banking sector’s excess liquidity remained captive, and did not spill out into the real economy, stoking inflation. Secondly, low credit growth reflected higher ‘net’ household saving, keeping the current account balance (CAB) strong (recall CAB = Saving - Investment). Thirdly, low credit growth meant that banks didn’t have to scramble for liquidity, thereby keeping deposit rates low; in fact, keeping deposit rates lower than bond yields incentivised domestic investors to move towards buying government bonds, helping fund the fiscal deficit.

But all of that could gradually change. Bank credit growth seems to be picking up across the board, steadily getting back to long-term averages, and could rise further if Bank Indonesia (BI) cuts rates in 2024. There is also substantial foreign direct investment (FDI) waiting on the side-lines, which could manifest once elections are over. USD30bn of foreign investment has already happened in the processed metals space over the last few years, with an equal amount waiting on the side-lines, as per our analysis of FDI intentions. Meanwhile, USD45bn of investment intentions have been announced in the EV space (i.e. batteries and autos). We forecast GDP growth to average 5.2% in 2024 versus 5.0% in 2023.

In fact, Indonesia is one of the economies where the next decade’s growth will likely be higher than the previous decade’s growth, as the economy climbs up the manufacturing value chain – from ores, to processed metals and EVs. In fact, we forecast that growth will accelerate by 0.5ppt over the medium term; a keen focus on macro stability will be central to that.

Due to a delayed hit to its export performance, Malaysia’s growth slowed notably in 2Q23, a reminder that no export-oriented economies could escape the global trade downturn unscathed. However, positive signs of recovery have emerged in 2H23, with higher-than-expected GDP growth of 3.3% y-o-y in 3Q23 – an impressive performance, as Malaysia saw a significantly high base of 14.1% y-o-y in 3Q22.

Granted, Malaysia is still grappling with a downturn in global trade. The manufacturing sector contracted by 0.1% y-o-y in 3Q23, a small downturn after a positive 0.1% growth in 2Q23. Trade also showed a similar trend, with exports declining by single digits in October. The weakness was mostly led by a sharp correction in global commodity markets, particularly oil, LNG and palm oil. But the nascent recovery in the global electronics cycle, as seen in peers like Korea and Singapore, provides some hope that Malaysia’s exports are seeing the light at the end of the tunnel. After all, consistent FDI continues to pour into Malaysia, making it still one of the top recipients in ASEAN. The added capacity should enable Malaysia’s manufacturing sector to rebound strongly when the trade cycle turns.

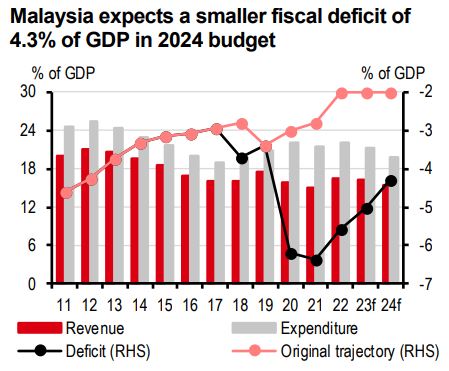

In addition to the green shoots in trade, Malaysia’s tourism-related sectors continue to provide much-needed support. In particular, Malaysia is among the frontrunners in ASEAN in attracting Chinese visitors. The tourism outlook has brightened further, after the recent announcement of China and Malaysia’s mutual visa exemption programme, making it more competitive among regional peers, not only in attracting tourists, but also potential investors. We recently raised our growth forecast to 4.1% (from 3.8%) for 2023 but retained our 2024 forecast at 4.5%, accounting for the better outturn in 3Q and a gradual uplift in the trade cycle.

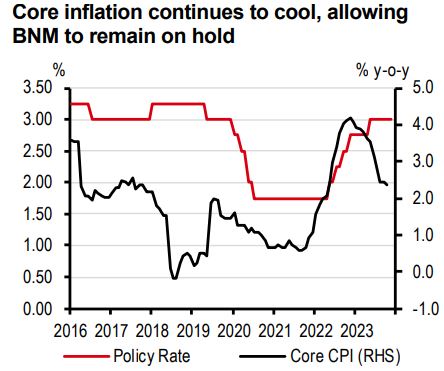

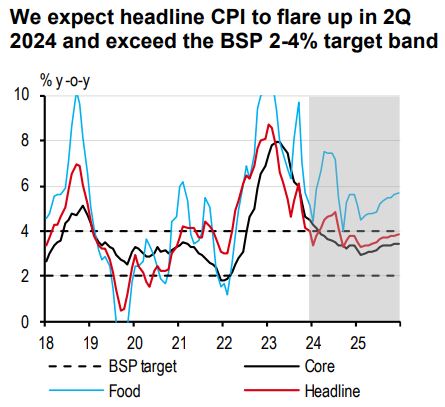

Meanwhile, inflation has been well contained. Headline inflation continued to cool in 3Q, to below 2% y-o-y, the second lowest rate in ASEAN, after Thailand. Quite positively, the impact from a recent rally in global rice prices has been partially blunted, thanks to the government’s efforts to ramp up domestic supply. But, upside risks to inflation remain, particularly from the changes in the 2024 budget, including a 2ppt hike in the services tax and some cuts to fuel subsidies. We forecast headline inflation of 2.5% for 2023 and 2.4% in 2024.

The Philippine economy still found momentum to run the engines in 3Q 2023, growing at 5.9% y-oy, well above what the market had expected. After this impressive clip, the archipelago is now well poised to become the fastest-growing ASEAN economy in 2023 despite seeing the fastest inflation rate and most aggressive monetary tightening. We recently raised our full-year GDP forecast for 2023 to 5.3% (from 4.8%) and acknowledged the archipelago’s robust display of resilience.

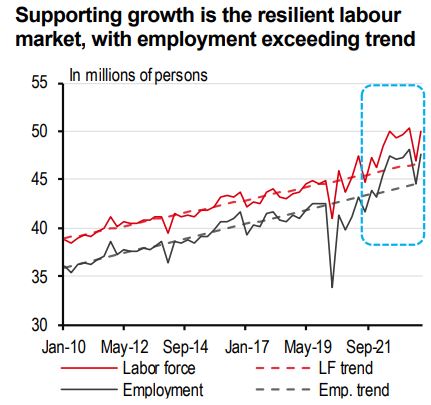

It helped that the Philippines was better insulated from the global headwinds relative to other economies. However, the main engine that kept the economy going was its people. The country’s labour market is currently booming with the unemployment rate the lowest in history, but with the labour force participation rate high. In absolute terms, there are roughly three million more people working compared to what the historical trend would suggest, with many using digitalization as leverage to seek employment in the informal sector. Yes, these jobs may not be the best in the world, but there is no doubt that what has been supporting growth amidst the challenges in 2023 was ‘strength in numbers,’ or having more hands on deck in the economy. And with a median age as young as 25 years old, this unique characteristic of demographic resilience should help buoy the Philippine economy for years to come.

This isn’t to say that the Philippines is in the clear. We still expect growth to come in softer than historical trend due to several domestic headwinds. For instance, headline CPI flared up in October as global rice prices surged, while monetary policy will likely remain tight to maintain balance in the economy. True, consumption by households and credit by large banks have been growing at their slowest pace since the Global Financial Crisis (barring the COVID-19 pandemic) and they have yet to enter their troughs. Investment, however, should continue to support growth with the government determined to continue its ambitious goal of spending 5% of GDP on infrastructure.

Although growth will likely be softer than usual, we don’t think the Bangko Sentral ng Pilipinas (BSP) will cut its policy rate anytime soon from 6.50%. Inflation will likely remain problematic until 2H 2024 while it is unlikely that the BSP cuts ahead of the Federal Reserve (Fed) to lend some support to the currency. We only expect the BSP to cut by 25bp after the Fed begins its easing cycle in 3Q 2024. We then expect the BSP to follow the Fed’s pace, cutting by 25bp in each quarter until the policy rate normalises at 5.00% by 4Q 2025.

After narrowly avoiding a technical recession in 2Q23, the worst seems to have passed for Singapore as its GDP rose by 1.4% q-o-q in 3Q23. More importantly, this growth has been broad-based.

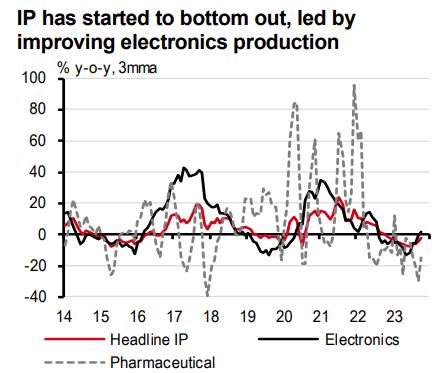

This is mostly evident in its key manufacturing sector, which has been in the doldrums for over a year. While external demand remains sluggish, the manufacturing sector saw its first sequential growth in 2023, though the magnitude was still marginal. In particular, a few green shoots appeared in electronics production, which grew double digits in October and November on average. While the recovery in the global electronics cycle is still at a nascent stage, it provides hope for tech-heavy economies of a key growth driver for 2024. Yet, we caution on the magnitude of the rebound.

Despite trade weakness, domestic demand provided much-needed support. After a few quarters of strength, private consumption still shows positive momentum from a tight labour market but reflects early signs of cooling from rising retrenchments. Also, travel-related services are driving growth, but with potential to improve further, as few sectors are yet to return to pre-pandemic levels. With the arrival of winter in the northern hemisphere, Singapore’s aviation industry is set to benefit sizeably. All in all, we forecast GDP growth of 1.2% for 2023 and 2.4% for 2024, on the back of an ongoing recovery in travel and a modest turn in the tech-led global trade cycle.

In addition, disinflation continues to be the dominant theme, with core inflation consistently cooling from its peak of 5.5% y-o-y to 3.3% y-o-y lately. However, October’s higher-thanexpected core inflation reminds the market that this remains sticky, and it is still a long process for inflation to decelerate to the Monetary Authority of Singapore’s (MAS) comfort zone. We forecast core inflation of 4.1% for 2023, but recently raised our 2024 forecast to 3.1% (from 2.9%) given upside risks from energy shocks and planned administrative hikes next year.

While the MAS will shift its focus from inflation to growth next year, imminent upside risks to inflation will constrain the MAS to start reversing its tightening cycle. We only expect the MAS to reduce its SGD Nominal Effective Exchange Rate (NEER) slope in April 2024 at the earliest.

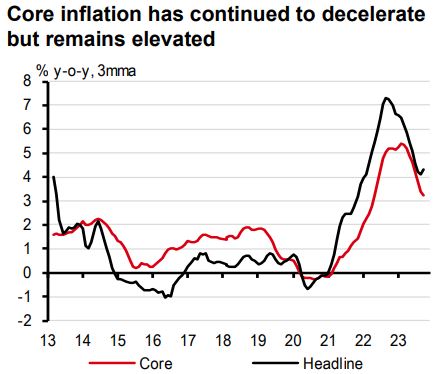

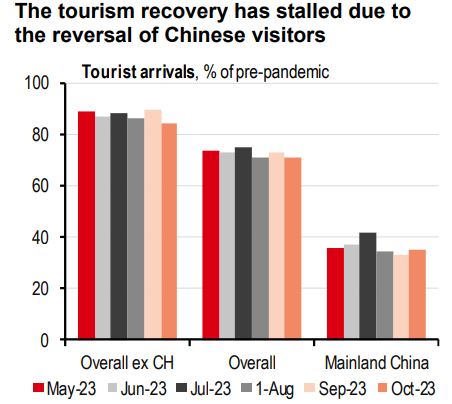

Many expected 2023 to be the year that the Land of Smiles would stage a strong recovery with the return of Chinese tourists, the economy’s biggest source of visitors, supporting the economy amidst Thailand’s election cycle. But the recovery of Chinese tourists wasn’t just slow. It even reversed midyear, leading to growth surprising to the downside for three consecutive quarters. Thailand also didn’t see its trade cycle turn as positively as its ASEAN peers. As a result, GDP is still below pre-pandemic levels, which is also reflected in the underperformance of its financial markets.

Will the Thai economy shake off its economic woes in 2024? Forward-looking indicators don’t look so promising. PMI new orders have plunged, the recovery of tourism has stalled, and exports to the US, Thailand’s top export destination, are expected to soften. The manufacturing production index (in terms of value) has fallen for 13 consecutive months due to competition from China and demand for hard disk drives falling – a structural issue the Thai economy has recently been grappling with. Travel sentiment from prospective Chinese tourists also remains weak as concerns over safety continue to linger. We don’t think the economy’s recovery is stuck, but it is pretty clear that Thailand’s export engine is sputtering.

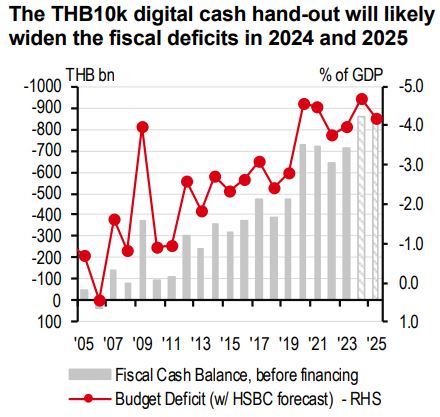

To get moving again, the authorities are looking to the economy’s domestic drivers for help. In the first four months in office, the new government has been generous in providing subsidies: diesel and gasoline prices were cut, electricity tariffs were lowered, sugar prices were controlled, and train fares were capped. This has resulted in headline CPI falling to negative territory, which, in turn, boosted consumption. In fact, the Bank of Thailand’s (BoT) private consumption index is growing near its fastest pace, barring the COVID-19 pandemic. And as its main policy for 2024, the government is determined to stimulate the economy and empower consumers through a THB10k digital cash handout scheme worth 2.6% of GDP. This should bolster consumption in the Year of the Dragon, and we expect growth to accelerate from 2.5% in 2023 to 3.8% in 2024. Other policies should also provide some fuel to growth, such as Thailand’s visa-free schemes to attract in tourists, as well as subsidies for electric vehicle production to spur investment.

Nonetheless, a fiscal stimulus of this size can stoke concerns over inflation. Mindful of this risk, we expect the BoT to stay pat and let fiscal policy do the work in supporting growth.

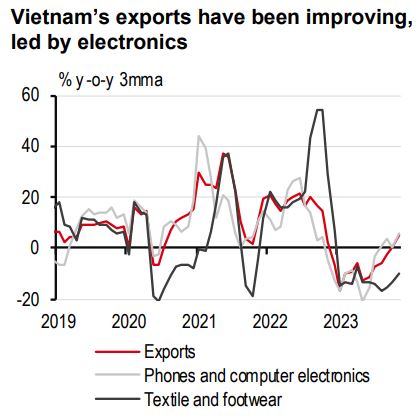

2023 was no doubt a tough year for Vietnam’s economy. Fortunately, the worst looks to have passed, as Vietnam’s GDP growth has recovered to 5.3% y-o-y in 3Q, from subdued growth of below-4% y-o-y in 1H. This is thanks to early signs of improving trade, which has strengthened into 4Q, though in part due to favourable base effects.

That said, the recovery is uneven. In particular, electronics shipments have been driving a gradual recovery in exports. However, other major exports, such as textiles and footwear, remain under pressure, leading to sizeable layoffs. For instance, Garmex Saigon Corporation, a textile giant, reportedly laid off 2,000 workers this year alone (VNExpress, 29 October). This suggests that it may take a while to see a broad-based recovery in trade.

However, a more gradual trade recovery does not mean a subdued investment landscape. In fact, newly registered manufacturing FDI is at record highs, a reflection of Vietnam’s ongoing attractiveness as a rising manufacturing hub. What is even more encouraging are signs of higher value-added manufacturing capability, exemplified by the inauguration of US-based Amkor’s USD1.6bn chip factory. One recent development that merits attention is Vietnam’s approval of a global minimum corporate tax of 15%, which will impact a handful of large multinational corporations (MNCs) in the manufacturing space.

Overall, we forecast 2023 GDP growth of 5.0%, but we recently trimmed our 2024 forecast to 6.0% (from 6.3%), given the uncertainty in the magnitude of a trade turnaround next year.

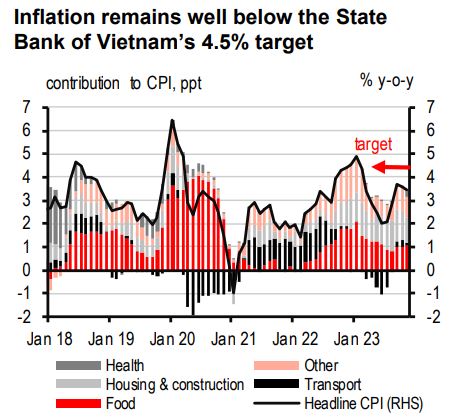

Meanwhile, inflation has been broadly in check, moderating to 3.5% y-o-y in November, well under the State Bank of Vietnam’s (SBV) 4.5% target. Despite lingering upside risks from food and energy, underlying price pressures are on a steady disinflation trajectory. Therefore, we expect inflation to come in around 3.3% in 2023 and 3.4% in 2024. This will warrant the SBV to stay put throughout our forecast horizon.

Important disclosures

Additional disclosures

1. This report is dated as at 15 December 2023.

2. All market data included in this report are dated as at close 14 December 2023, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of a financial instrument or of an investment fund.

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Bank Canada, HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (200801006421 (807705-X)), The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, HSBC Private Bank Suisse SA, South Africa Representative Office, HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA and The Hongkong and Shanghai Banking Corporation Limited (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/business. However, the Bank disclaims any guaranty on the management or operation performance of the trust business.

The following statement is only applicable to by HSBC Bank Australia with regard to how the publication is distributed to its customers: This document is distributed by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL/ACL 232595 (HBAU). HBAP has a Sydney Branch ARBN 117 925 970 AFSL 301737.The statements contained in this document are general in nature and do not constitute investment research or a recommendation, or a statement of opinion (financial product advice) to buy or sell investments. This document has not taken into account your personal objectives, financial situation and needs. Because of that, before acting on the document you should consider its appropriateness to you, with regard to your objectives, financial situation, and needs.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

Mainland China

In mainland China, this document is distributed by HSBC Bank (China) Company Limited (“HBCN”) and HSBC FinTech Services (Shanghai) Company Limited to its customers for general reference only. This document is not, and is not intended to be, for the purpose of providing securities and futures investment advisory services or financial information services, or promoting or selling any wealth management product. This document provides all content and information solely on an "as-is/as-available" basis. You SHOULD consult your own professional adviser if you have any questions regarding this document.

The material contained in this document is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HSBC India does not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investments are subject to market risk, read all investment related documents carefully.

© Copyright 2023. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes.

There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks. In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.